Introduction

Every business tells a story through its numbers. And at the heart of that story lies operating profit—a figure that reveals how well a company truly runs its core operations.

If revenue is the applause and net income is the curtain call, operating profit is the performance itself. It shows whether a company can generate earnings from what it actually does, without relying on financial tricks, tax strategies, or one-off events. For entrepreneurs, investors, managers, and students, understanding this metric isn’t optional—it’s essential.

Why does this matter to you? Because operating performance determines sustainability. A company with strong sales but weak cost control may look successful on the surface, yet struggle underneath. Knowing how to interpret this figure can change how you view businesses, investments, and even your own financial decisions.

What Is Operating Profit?

In simple terms, operating profit is the amount a company earns from its core business activities after deducting operating expenses.

It excludes:

- Interest expenses

- Taxes

- Gains or losses from investments

- One-time or extraordinary items

This makes it a pure measure of operational efficiency.

After revenue comes in, businesses must pay for:

- Cost of goods sold (COGS)

- Salaries and wages

- Rent

- Utilities

- Marketing

- Administrative costs

What remains after these costs—but before interest and taxes—is operating profit.

Illustration of income statement components including revenue and expenses

Why It Matters

This metric answers a critical question:

Is the company’s core business model profitable?

A business might report high net income due to tax advantages or investment gains. But if operating profit is weak, the underlying operations may be unstable.

For managers, this figure highlights efficiency.

For investors, it signals operational strength.

For lenders, it reflects repayment capacity.

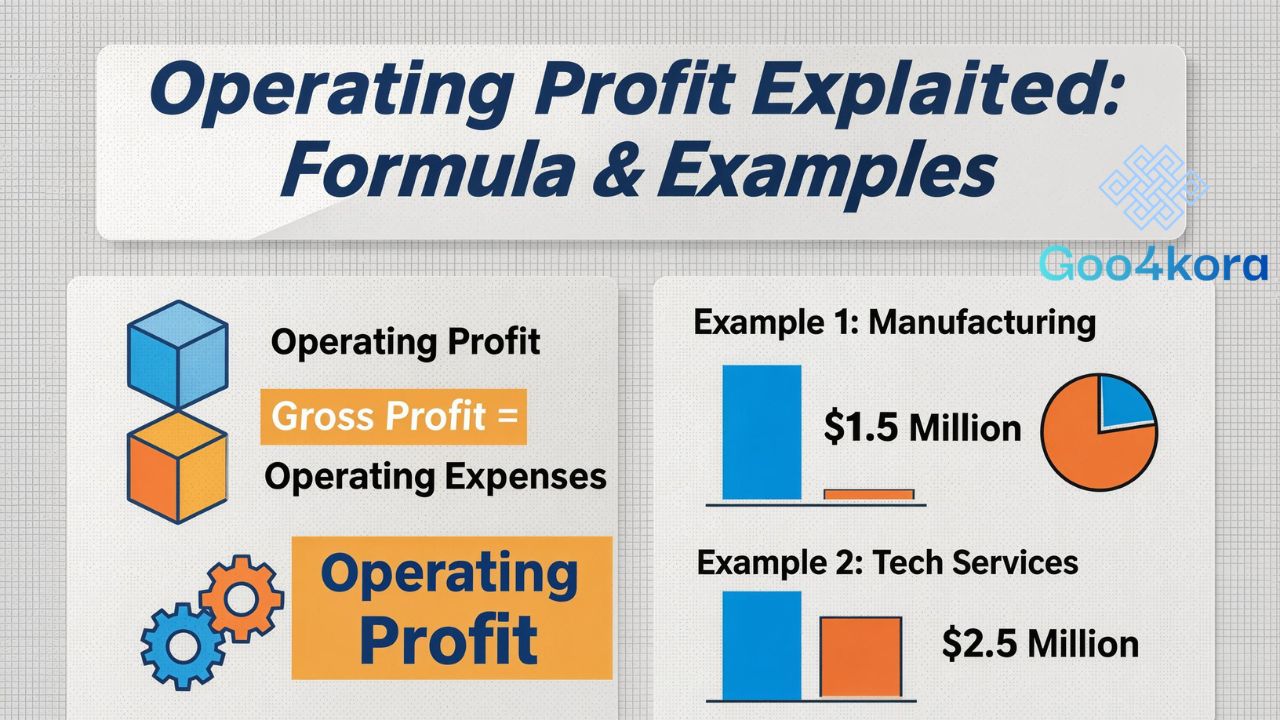

How to Calculate Operating Profit

The formula is straightforward:

Operating Profit = Gross Profit – Operating Expenses

Or expanded:

Operating Profit = Revenue – COGS – Operating Expenses

Where:

- Revenue is total sales.

- COGS includes direct production costs.

- Operating expenses include overhead and administrative costs.

Step-by-Step Example

Imagine a company reports:

- Revenue: $500,000

- Cost of Goods Sold: $300,000

- Operating Expenses: $120,000

First calculate gross profit:

$500,000 – $300,000 = $200,000

Then subtract operating expenses:

$200,000 – $120,000 = $80,000

The operating profit is $80,000.

This means the business generated $80,000 from its primary activities before interest and taxes.

Financial calculations showing revenue and cost structure

Operating Profit vs. Gross Profit vs. Net Profit

Many people confuse these terms. Let’s break them down clearly.

Gross Profit

Gross profit only subtracts the cost of producing goods or services from revenue. It does not include overhead.

Formula:

Revenue – COGS

It tells you how efficiently products are made.

Operating Profit

This subtracts both production costs and operating expenses.

It reflects how well the entire operation runs—not just production.

Net Profit

Net profit is what remains after:

- Interest

- Taxes

- Non-operating income/expenses

It represents the final bottom-line earnings.

Understanding the distinction is vital. A company may have strong gross profit but weak operating profit due to excessive administrative spending.

What Affects Operating Profit?

Several factors influence this figure.

1. Revenue Growth

Increasing sales without proportionally increasing costs boosts operating performance.

2. Cost Control

Reducing waste, renegotiating supplier contracts, and improving efficiency can significantly raise operating profit.

3. Pricing Strategy

Premium pricing may improve margins—but only if customers perceive value.

4. Economies of Scale

As production increases, fixed costs are spread over more units, improving profitability.

5. Operational Efficiency

Automation, better processes, and improved workforce productivity can increase margins without raising revenue.

Operating Profit Margin: A Key Performance Indicator

To compare companies of different sizes, we use operating profit margin.

Formula:

Operating Profit Margin = Operating Profit ÷ Revenue × 100

This percentage shows how much profit is generated per dollar of revenue.

For example:

If operating profit is $80,000 and revenue is $500,000:

80,000 ÷ 500,000 × 100 = 16%

A 16% margin means the company keeps 16 cents from every dollar of sales after covering operating costs.

Why Margin Matters

Absolute numbers can be misleading. A large company may earn millions in operating profit but have a low margin. A smaller company might earn less but operate more efficiently.

Margins allow meaningful comparison across industries and competitors.

Operating Profit in Financial Analysis

Financial analysts rely heavily on operating profit because it removes external distortions.

It Helps Assess:

- Operational efficiency

- Cost management

- Pricing power

- Sustainability of earnings

Investors often look at trends over multiple years. A rising figure indicates improving efficiency. A declining one may signal operational trouble.

EBIT and Operating Profit

You may hear the term EBIT (Earnings Before Interest and Taxes). In most cases, EBIT and operating profit are used interchangeably, though slight accounting differences can exist.

Both focus on core operational performance.

Industry Benchmarks and Variations

Different industries have different expectations.

- Retail: Often 5–10% margin

- Technology: Can exceed 20%

- Manufacturing: Typically 10–15%

- Airlines: Often low single digits

A “good” operating profit depends on the industry context. Comparing a grocery store to a software company makes little sense without considering structural cost differences.

How Businesses Improve Operating Profit

Improvement strategies fall into two broad categories: increasing revenue or reducing costs.

Revenue-Focused Strategies

- Upselling and cross-selling

- Entering new markets

- Launching premium products

- Improving customer retention

Cost-Focused Strategies

- Process automation

- Outsourcing non-core functions

- Lean management practices

- Energy efficiency programs

Smart businesses balance both approaches.

Common Mistakes When Interpreting Operating Profit

Even experienced professionals sometimes misread the numbers.

1. Ignoring One-Time Expenses

A temporary expense spike can distort annual performance.

2. Failing to Compare Over Time

One year’s data is not enough. Trends reveal the true picture.

3. Overlooking Industry Norms

Margins vary significantly by sector.

4. Confusing Cash Flow with Profit

Operating profit is not the same as cash flow. A profitable company can still face liquidity problems.

Operating Profit and Business Decision-Making

Executives use this figure when:

- Setting budgets

- Evaluating departments

- Making expansion decisions

- Determining performance bonuses

Investors use it to:

- Compare companies

- Assess management effectiveness

- Forecast future earnings

Banks consider it when assessing loan eligibility, as it reflects repayment capacity from operations.

Real-World Scenario

Consider two companies with identical revenue of $10 million.

Company A:

- High marketing spend

- Inefficient supply chain

- Outdated technology

Company B:

- Automated systems

- Optimized sourcing

- Tight cost controls

Even with the same revenue, Company B will likely report stronger operating profit. The difference lies in operational discipline—not sales alone.

FAQ

Frequently Asked Questions

What is operating profit in simple terms?

It is the money a business earns from its main activities after covering operating expenses but before paying interest and taxes.

Is operating profit the same as EBIT?

In most financial reporting contexts, yes. Both represent earnings before interest and taxes, focusing on operational performance.

Why is operating profit important for investors?

It shows how efficiently a company runs its core business, helping investors evaluate sustainability and growth potential.

How is operating profit different from net profit?

Net profit includes interest, taxes, and non-operating items. Operating profit focuses only on core business operations.

Can a company have positive net profit but low operating profit?

Yes. Investment gains or tax advantages may boost net profit even if operational performance is weak.

What does a declining operating profit indicate?

It may signal rising costs, pricing pressure, inefficiencies, or declining sales performance.

Is a higher operating profit always better?

Generally yes, but it must be evaluated relative to revenue, industry benchmarks, and long-term sustainability.

How often should businesses analyze operating profit?

Most companies review it quarterly and annually, but internal monitoring often happens monthly.

Conclusion

Understanding operating profit transforms how you evaluate a business. It strips away financial noise and focuses on what truly matters: how well a company performs at its core.

Revenue can impress. Net income can excite. But operating profit reveals discipline, efficiency, and operational strength.

Whether you are an investor comparing stocks, an entrepreneur managing costs, or a student learning financial fundamentals, mastering this metric gives you a clearer lens through which to view business success.