Introduction

Money moves fast in business—but how do you keep track of where it comes from and where it goes? That’s where the accounting equation becomes your most powerful tool. It’s simple, elegant, and forms the backbone of every financial statement you’ve ever seen.

If you’ve ever wondered how companies know exactly what they own, what they owe, and what truly belongs to them, the answer lies in this one foundational formula. Whether you’re a student, entrepreneur, investor, or simply curious about finance, understanding the accounting equation gives you clarity and control.

In this guide, we’ll break it down step by step. No jargon overload. No unnecessary complexity. Just practical explanations, real-life examples, and a deep understanding you can actually use.

What Is the Accounting Equation?

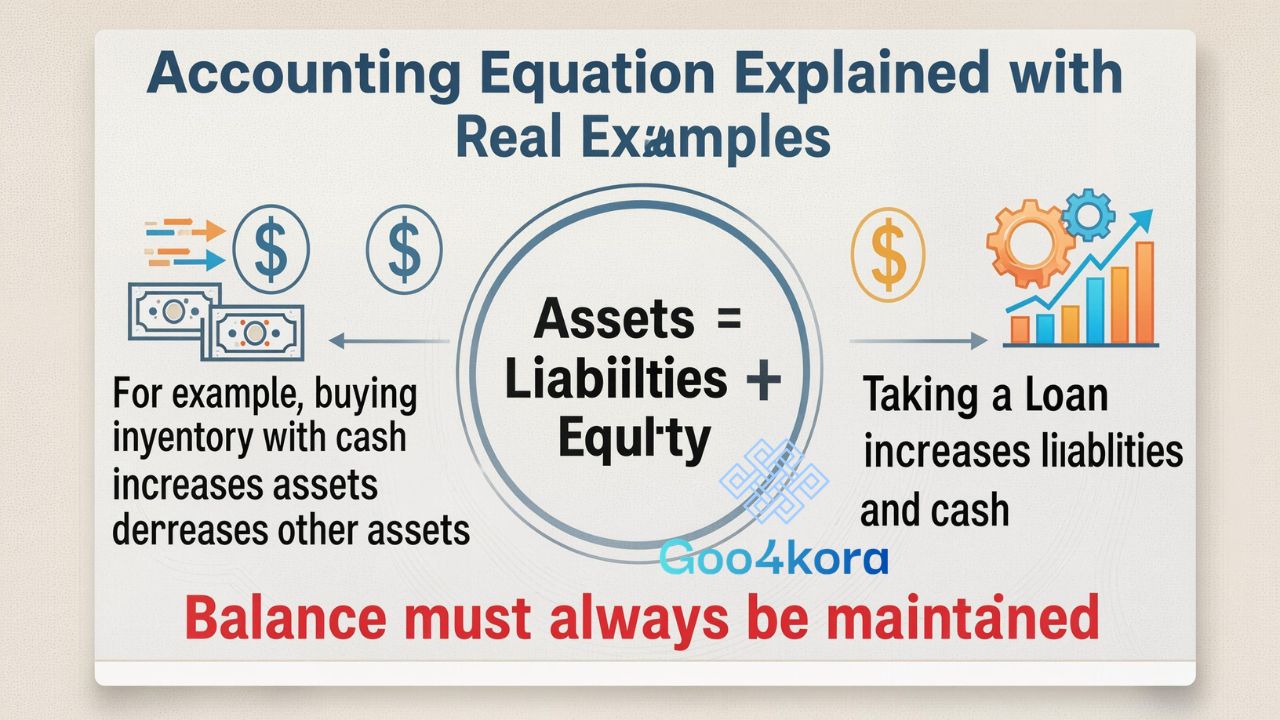

At its core, the accounting equation is:

Assets = Liabilities + Equity

This formula represents the relationship between what a business owns and how those assets are financed.

- Assets are resources owned by the business.

- Liabilities are obligations or debts.

- Equity represents the owner’s residual interest.

This equation must always stay balanced. Every financial transaction affects at least two accounts to keep both sides equal. That’s the foundation of double-entry bookkeeping.

After all, accounting isn’t about numbers—it’s about balance.

Breaking Down Each Component

Assets: What the Business Owns

Assets are economic resources with value. They can be tangible or intangible.

Common examples include:

- Cash

- Inventory

- Equipment

- Buildings

- Accounts receivable

- Patents

Assets are typically divided into:

- Current assets (cash, receivables, inventory)

- Non-current assets (property, plant, equipment)

If it provides future economic benefit, it likely qualifies as an asset.

Liabilities: What the Business Owes

Liabilities are financial obligations. These are amounts owed to lenders, suppliers, or other creditors.

Examples include:

- Bank loans

- Accounts payable

- Salaries payable

- Taxes owed

- Mortgage obligations

Like assets, liabilities are categorized into:

- Current liabilities (due within one year)

- Long-term liabilities (due after one year)

Liabilities represent external claims on company assets.

Equity: The Owner’s Claim

Equity is what remains after liabilities are deducted from assets.

Rewriting the accounting equation:

Equity = Assets − Liabilities

Equity includes:

- Owner’s capital

- Retained earnings

- Additional paid-in capital

In simple terms, equity is the net worth of the business.

Why the Accounting Equation Matters

The accounting equation is not just a classroom formula. It shapes:

- The balance sheet

- The double-entry accounting system

- Financial statement accuracy

- Business valuation

- Investor analysis

Every single transaction—whether buying equipment, paying salaries, or earning revenue—affects this equation.

If the equation doesn’t balance, something is wrong.

That’s why accountants rely on it daily. It’s the structural foundation of modern accounting systems worldwide.

How Transactions Affect the Accounting Equation

Let’s look at simple scenarios.

Example 1: Owner Invests Cash

Sarah starts a business and invests $10,000 cash.

- Assets increase by $10,000 (cash)

- Equity increases by $10,000 (owner’s capital)

Equation remains balanced.

Example 2: Business Takes a Loan

The company borrows $5,000 from a bank.

- Assets increase by $5,000 (cash)

- Liabilities increase by $5,000 (loan payable)

Still balanced.

Example 3: Buying Equipment with Cash

The business buys equipment worth $2,000.

- Equipment increases

- Cash decreases

Total assets remain the same.

The Expanded Accounting Equation

As businesses grow, the basic equation expands to reflect income and expenses.

Expanded version:

Assets = Liabilities + Owner’s Equity + Revenue − Expenses − Drawings

Why expand it?

Because revenue increases equity.

Expenses decrease equity.

Owner withdrawals reduce equity.

This expanded form helps explain how income statements connect to the balance sheet.

Relationship Between the Accounting Equation and the Balance Sheet

The balance sheet is essentially the accounting equation presented in report format.

Left side:

- Assets

Right side:

- Liabilities

- Equity

The totals must always match.

If they don’t, either:

- A transaction was recorded incorrectly

- An entry was omitted

- A calculation error occurred

The accounting equation ensures structural integrity.

Real-World Business Example

Imagine a small café.

Starting Position:

Owner invests $20,000.

Assets = $20,000 cash

Equity = $20,000

Café Buys Equipment for $8,000 (cash)

Cash decreases.

Equipment increases.

Total assets unchanged.

Café Takes $5,000 Loan

Assets increase (cash).

Liabilities increase (loan).

Café Earns $3,000 Revenue

Cash increases.

Equity increases.

Café Pays $1,000 Expenses

Cash decreases.

Equity decreases.

At every stage, the accounting equation holds true.

Common Mistakes When Using the Accounting Equation

Even experienced professionals sometimes make errors. Common issues include:

- Forgetting double-entry rules

- Misclassifying assets as expenses

- Recording revenue prematurely

- Ignoring accrued liabilities

- Confusing equity with profit

The key is remembering that every transaction has two sides.

If the equation doesn’t balance, revisit the entries.

How the Accounting Equation Supports Financial Analysis

Investors and analysts rely on this formula to:

- Measure financial stability

- Evaluate debt levels

- Assess solvency

- Calculate net worth

- Understand capital structure

For example:

High liabilities relative to assets may indicate financial risk.

Strong equity growth suggests healthy profitability.

Everything starts with the accounting equation.

The Role in Double-Entry Bookkeeping

The accounting equation exists because of double-entry accounting.

Every transaction:

- Debits one account

- Credits another

Debits and credits ensure the equation remains balanced.

Without this structure, financial statements would be unreliable.

Accounting Equation in Modern Software

Today’s accounting software automates calculations. But behind every click:

- The equation still operates

- Balance checks still occur

- Transactions still follow double-entry rules

Even advanced ERP systems are built on this simple foundation.

Technology changed the tools—but not the logic.

Advanced Insight: Owner’s Equity Changes Over Time

Equity evolves due to:

- Net income

- Dividends or drawings

- Additional investments

- Share issuance

Understanding these movements helps business owners track growth.

The accounting equation visually demonstrates how profit accumulates within equity.

How Students Can Master the Accounting Equation

Here’s a practical approach:

- Memorize the formula.

- Practice transaction analysis daily.

- Use T-accounts for clarity.

- Always check balance.

- Solve real-life business scenarios.

Repetition builds intuition.

Eventually, you’ll start seeing every business event through the lens of this equation.

Frequently Asked Questions

FAQ

What is the basic accounting equation?

The accounting equation states that assets equal liabilities plus equity. It shows how resources are financed.

Why must the accounting equation always balance?

Because every transaction affects at least two accounts. Double-entry bookkeeping ensures equality on both sides.

What happens if the equation doesn’t balance?

It usually means there is an accounting error such as a missing entry or incorrect classification.

Is the accounting equation used in small businesses?

Yes. From startups to multinational corporations, the same principle applies universally.

How does revenue affect the accounting equation?

Revenue increases equity because it increases retained earnings.

How do expenses affect the accounting equation?

Expenses decrease equity since they reduce net income.

What is the expanded accounting equation?

It includes revenue, expenses, and drawings to show detailed equity changes.

Does accounting software use this equation?

Absolutely. Every modern accounting system relies on it behind the scenes.

Conclusion

The accounting equation may look simple at first glance, but it holds extraordinary power. It keeps businesses accountable, financial statements accurate, and investors informed.

Once you understand how assets, liabilities, and equity interact, you start seeing financial data differently. Every transaction tells a story. Every number connects.

Master this one principle, and you unlock the language of business itself.