Introduction

Imagine spending decades building wealth—buying property, growing investments, and creating financial security for your family—only to see a large portion disappear due to estate taxes. That’s a real concern for many families planning their legacy. This is where a credit shelter trust becomes a powerful tool.

A credit shelter trust is an estate planning strategy designed to protect wealth, minimize estate taxes, and ensure assets pass efficiently to future generations. For married couples with significant estates, it can be one of the most effective ways to preserve family wealth.

However, many people misunderstand how this trust works. Some believe it’s only for the ultra-wealthy, while others assume it’s overly complex. In reality, when structured properly, it can be a straightforward yet powerful financial planning tool.

In this guide, we’ll break down everything you need to know—from how a credit shelter trust works to its benefits, setup process, and real-life examples. By the end, you’ll understand why financial planners and estate attorneys often recommend it for long-term wealth protection.

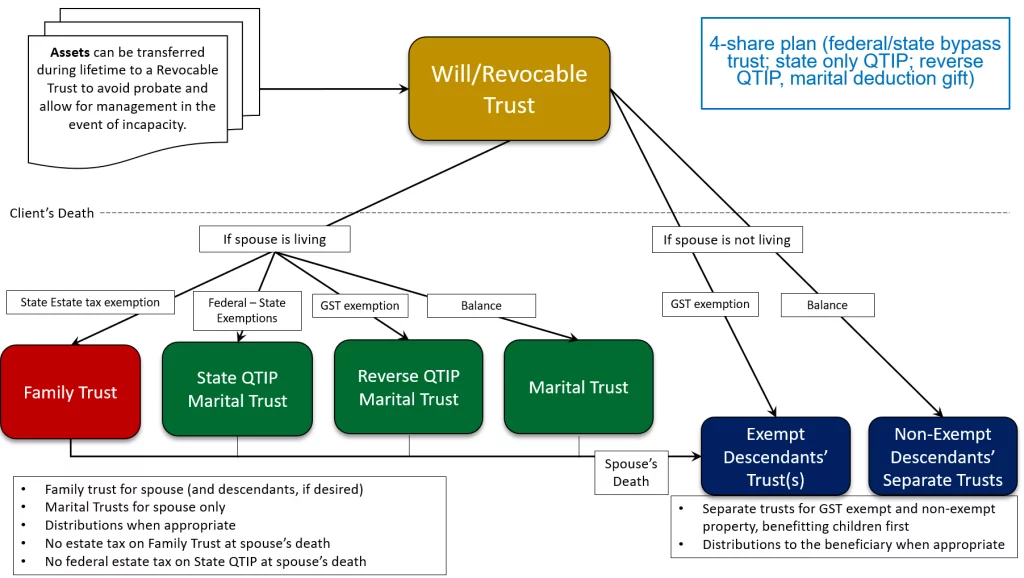

What Is a Credit Shelter Trust

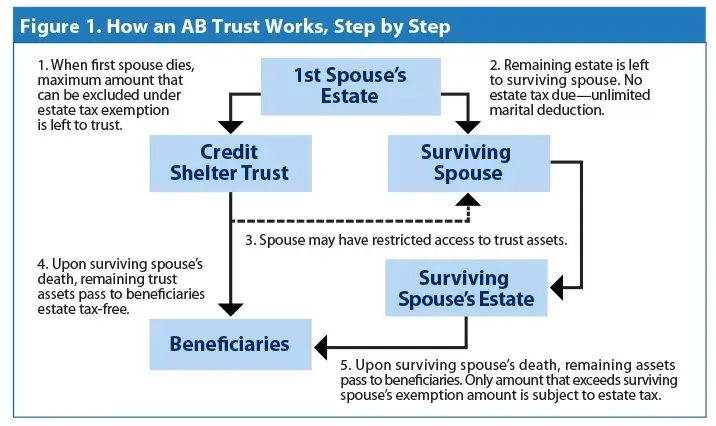

A credit shelter trust is an irrevocable trust created by married couples to reduce estate taxes when one spouse passes away. It allows couples to fully utilize their estate tax exemptions and transfer wealth to heirs with minimal tax burden.

In simple terms, the trust “shelters” assets from estate taxation when the surviving spouse dies.

Without proper estate planning, a large portion of inherited wealth may become subject to federal estate taxes. In the United States, estate tax exemptions exist, but failing to structure assets strategically could mean losing millions in taxes.

A credit shelter trust—sometimes called a bypass trust or family trust—ensures each spouse’s exemption is fully used.

Basic Definition

A credit shelter trust is:

- A trust activated after the first spouse dies

- Funded with assets equal to the estate tax exemption

- Designed to pass wealth to heirs tax-efficiently

The surviving spouse can still benefit from the trust’s income or assets, but those assets are excluded from the surviving spouse’s taxable estate.

How a Credit Shelter Trust Works

Understanding how this estate planning tool functions is easier with a step-by-step explanation.

Step 1: Creation of the Trust

A married couple establishes a trust as part of their estate plan. The trust typically becomes active upon the death of the first spouse.

Step 2: Funding the Trust

When the first spouse dies, assets up to the estate tax exemption limit are placed into the credit shelter trust.

These assets may include:

- Investment portfolios

- Real estate

- Business interests

- Cash accounts

Step 3: Benefits for the Surviving Spouse

The surviving spouse can receive:

- Income generated by trust assets

- Limited access to principal

- Financial support if necessary

However, the assets themselves are no longer part of the surviving spouse’s estate.

Step 4: Transfer to Heirs

When the surviving spouse passes away, trust assets transfer to beneficiaries—usually children—without being taxed again as part of the estate.

History and Purpose of Credit Shelter Trusts

Estate planning strategies evolved alongside tax laws. The credit shelter trust became popular after the United States introduced federal estate taxes in the early 20th century.

Before portability rules existed, many married couples unintentionally wasted one spouse’s estate tax exemption.

For example:

If a couple had $20 million in assets and only one spouse’s exemption was used, the remaining wealth could face heavy taxation.

A credit shelter trust solved this problem by preserving both exemptions.

Today, even with portability laws allowing transfer of exemptions between spouses, many financial advisors still recommend these trusts because they offer additional protections.

Key Components of a Credit Shelter Trust

Several elements make this estate planning structure effective.

Trust Grantor

The individuals who create the trust—usually a married couple.

Trustee

The trustee manages assets inside the trust and ensures they follow the trust’s terms.

Trustees can include:

- Family members

- Attorneys

- Financial institutions

Beneficiaries

Beneficiaries are the individuals who ultimately receive trust assets.

Common beneficiaries include:

- Children

- Grandchildren

- Other family members

Trust Assets

Assets placed in the trust may include:

| Asset Type | Example |

|---|---|

| Real Estate | Homes or rental properties |

| Investments | Stocks, bonds, ETFs |

| Business Ownership | Private company shares |

| Cash | Savings accounts |

Benefits of a Credit Shelter Trust

There are several reasons estate planners recommend this strategy.

Estate Tax Reduction

One of the biggest advantages is tax savings.

By utilizing both spouses’ exemptions, families can potentially protect millions of dollars from estate taxes.

Asset Protection

Trust assets are typically protected from:

- Creditors

- Lawsuits

- Financial mismanagement by heirs

Control Over Inheritance

The trust allows the original owners to specify how and when heirs receive assets.

For example:

- Children receive funds at age 30

- Education expenses are covered first

- Assets distributed gradually

Wealth Preservation Across Generations

This strategy helps families maintain generational wealth.

Many high-net-worth families rely on trust structures to ensure financial stability for future generations.

Potential Drawbacks and Limitations

Despite its advantages, this trust structure also has limitations.

Irrevocable Structure

Once assets are placed inside the trust, changes can be difficult.

Legal and Administrative Costs

Creating and maintaining a trust may involve:

- Attorney fees

- Administrative expenses

- Tax filings

Limited Access for the Surviving Spouse

Although the surviving spouse benefits from the trust, their access to principal may be restricted.

Credit Shelter Trust vs Other Trust Structures

Estate planning includes many different types of trusts.

Below is a comparison table.

| Trust Type | Purpose | Flexibility |

|---|---|---|

| Revocable Living Trust | Avoid probate | High |

| Irrevocable Trust | Asset protection | Low |

| Marital Trust | Benefit surviving spouse | Moderate |

| Credit Shelter Trust | Estate tax reduction | Moderate |

Unlike a simple revocable trust, a credit shelter trust specifically focuses on tax efficiency.

Who Should Consider a Credit Shelter Trust

Not every family needs this estate planning structure.

However, it may be ideal for:

- Couples with large estates

- Families owning businesses

- Individuals with multiple properties

- High-net-worth investors

Financial planners often recommend this trust for estates approaching or exceeding estate tax thresholds.

Real-Life Example of a Credit Shelter Trust

Let’s consider a simplified scenario.

John and Maria have an estate worth $25 million.

Without proper planning:

- John dies first

- Maria inherits everything

- When Maria dies, the entire estate may face estate taxes

With a credit shelter trust:

- John’s exemption funds the trust

- Maria receives income from trust assets

- Remaining estate taxes are reduced significantly

Over time, this structure could save millions of dollars.

Personal Background of Estate Planning Strategies

Estate planning has evolved dramatically over the past century.

In the early 1900s, wealthy industrialists and business owners began using trusts to manage inheritance and reduce taxes.

Financial advisors, estate attorneys, and wealth managers later refined these strategies to support families across multiple generations.

Today, estate planning is a sophisticated financial discipline combining:

- Legal frameworks

- Investment management

- Tax strategies

Large financial institutions manage trillions of dollars in trust assets worldwide, highlighting how essential structured wealth planning has become.

Modern families—especially entrepreneurs, property investors, and business owners—use trusts not just for tax savings but also for protecting legacy.

FAQ

What is a credit shelter trust used for?

A credit shelter trust is primarily used to reduce estate taxes and preserve family wealth by utilizing both spouses’ estate tax exemptions.

Is a credit shelter trust the same as a bypass trust?

Yes. A bypass trust is another name for a credit shelter trust. Both terms refer to the same estate planning strategy.

Who manages a credit shelter trust?

A trustee manages the trust. This can be a family member, professional trustee, attorney, or financial institution.

Can the surviving spouse access the trust assets?

Yes, but access is usually limited to income or specific financial needs depending on the trust’s terms.

Is a credit shelter trust still necessary today?

Although estate tax portability exists, many advisors still recommend credit shelter trusts for asset protection and better control of inheritance.

What assets can be placed in a credit shelter trust?

Common assets include real estate, investment accounts, business interests, and cash savings.

How much does it cost to set up a credit shelter trust?

Costs vary depending on complexity but may range from a few thousand dollars to more for advanced estate planning.

Can a credit shelter trust be changed?

Generally, these trusts are irrevocable once activated, meaning changes may be difficult or impossible.

Conclusion

Planning how your wealth will be transferred after you’re gone can feel uncomfortable, but it’s one of the most important financial decisions you’ll ever make. A credit shelter trust offers a strategic way to preserve family assets, minimize estate taxes, and ensure your legacy supports future generations.

For couples with significant assets, this trust structure can provide peace of mind knowing their wealth won’t be unnecessarily reduced by taxes. By combining tax efficiency, asset protection, and inheritance control, it remains one of the most powerful estate planning tools available.

However, like any financial strategy, it should be designed carefully with the help of experienced estate attorneys and financial planners. When done correctly, a credit shelter trust can transform decades of hard work into lasting generational wealth.