Introduction

Cryptocurrency feels like freedom—fast, decentralized, and private. But then reality hits: taxes. And suddenly, the big question pops up—does coinbase report to irs?

If you’ve ever bought, sold, or traded crypto on Coinbase, you’re not alone in wondering how much the IRS actually knows. It’s a fair concern. After all, crypto started with anonymity in mind, but regulations have evolved quickly.

Understanding how Coinbase interacts with the IRS isn’t just about avoiding penalties—it’s about staying informed, confident, and in control of your financial future. Let’s break it down in a way that actually makes sense.

Understanding Coinbase and IRS Reporting

Before diving deeper, let’s clarify what Coinbase actually is.

Coinbase is one of the largest cryptocurrency exchanges in the world, especially popular in the United States. It allows users to:

- Buy and sell cryptocurrencies

- Store digital assets

- Trade coins like Bitcoin, Ethereum, and more

Now here’s where things get serious—Coinbase operates as a regulated financial platform. That means it must follow U.S. laws, including tax reporting requirements.

So when people ask, “does coinbase report to irs,” the answer isn’t just yes or no—it depends on several factors, which we’ll unpack next.

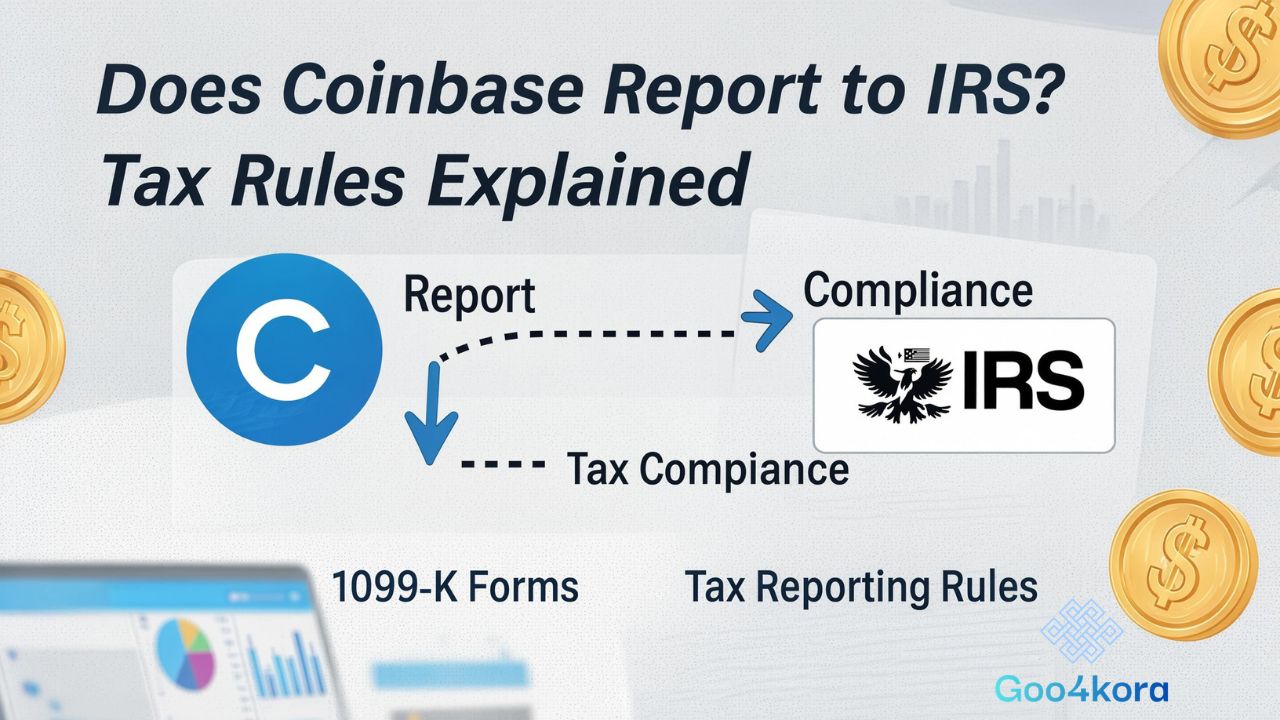

Does Coinbase Report to IRS Directly?

The short answer: Yes, Coinbase does report certain information to the IRS.

However, it’s not as simple as sending every transaction detail automatically.

How it works in reality:

- Coinbase does not report every single trade automatically to the IRS

- But it does report specific user data and tax forms depending on your activity

- The IRS can also request additional information directly from Coinbase

This means your crypto activity is not invisible.

In fact, the IRS has already taken legal action in the past to obtain user data from Coinbase, which tells you everything about how seriously they treat crypto taxes.

What Information Coinbase Shares with the IRS

When evaluating “does coinbase report to irs,” it’s important to understand what is actually shared.

Coinbase may report:

- Your name, address, and account details

- Transaction history (in certain cases)

- Total earnings or rewards

- Gains from specific activities

What’s NOT always directly reported:

- Every buy/sell trade automatically

- Detailed capital gains calculations

That said, don’t assume you’re under the radar. The IRS uses advanced tracking tools and blockchain analytics to connect the dots.

IRS Forms You May Receive from Coinbase

Coinbase issues specific tax forms depending on your activity level.

Common forms include:

1. Form 1099-MISC

You may receive this if:

- You earned $600 or more from staking, rewards, or referrals

2. Form 1099-B (limited rollout)

- Reports proceeds from crypto sales

- Still evolving and not always issued to all users

3. Account Statements

- Detailed transaction history for your own reporting

Important note:

Even if you don’t receive a form, you are still responsible for reporting your crypto taxes.

This is where many people make a mistake—they assume no form means no obligation. That’s simply not true.

Crypto Transactions That Trigger Taxes

To fully understand does coinbase report to irs, you need to know what actually counts as a taxable event.

Taxable crypto events include:

- Selling crypto for cash

- Trading one cryptocurrency for another

- Using crypto to purchase goods/services

- Earning crypto through staking or mining

Non-taxable events:

- Buying crypto with cash

- Transferring crypto between your own wallets

Example:

Let’s say you bought Bitcoin at $20,000 and sold it at $30,000.

- Your profit: $10,000

- This is a taxable capital gain

How the IRS Tracks Cryptocurrency Activity

Even if you’re still wondering “does coinbase report to irs,” here’s the bigger picture:

The IRS doesn’t rely solely on Coinbase.

They use:

- Blockchain analysis tools

- Data-sharing agreements

- Exchange compliance reports

- Audit trails from financial accounts

In fact, since 2020, the IRS has included a direct question on tax returns:

“Did you receive, sell, send, exchange, or acquire any financial interest in virtual currency?”

That alone tells you how serious enforcement has become.

Consequences of Not Reporting Coinbase Taxes

Ignoring crypto taxes might feel tempting—but it can get expensive fast.

Possible consequences:

- Penalties and fines

- Interest on unpaid taxes

- IRS audits

- Legal action in severe cases

Real talk:

The IRS isn’t chasing small mistakes aggressively, but intentional non-reporting is a different story.

If you’re using Coinbase regularly, it’s safer to assume your activity is visible.

How to Stay Compliant with Crypto Taxes

Now that we’ve answered “does coinbase report to irs,” let’s focus on what you should actually do.

Step-by-step compliance guide:

1. Track every transaction

Use tools like:

- CoinTracker

- Koinly

- TaxBit

2. Calculate gains and losses

You need to determine:

- Cost basis

- Sale price

- Profit or loss

3. Report on your tax return

Include:

- Capital gains (Schedule D)

- Income from crypto (Schedule 1 or C)

4. Keep records

Hold onto:

- Trade history

- Wallet transfers

- Exchange statements

Real-Life Example: A Coinbase User’s Tax Scenario

Let’s make this real.

Ali, a freelance designer, started investing in crypto through Coinbase in 2022.

His activity:

- Bought Ethereum worth $2,000

- Sold it later for $3,500

- Earned $800 from staking

Tax implications:

| Activity | Amount | Tax Type |

|---|---|---|

| ETH Sale Profit | $1,500 | Capital Gain |

| Staking Rewards | $800 | Ordinary Income |

Even if Ali didn’t ask, “does coinbase report to irs,” his data may still be partially visible.

If he fails to report:

- He risks penalties

- The IRS may flag discrepancies later

Personal Background: The Rise of Crypto Investors

Crypto investors today come from all walks of life—students, freelancers, engineers, even retirees.

Typical journey:

- Start with curiosity (Bitcoin headlines)

- Open Coinbase account

- Make first investment

- Gradually expand portfolio

Achievements:

- Early adopters saw massive returns

- Some turned small investments into life-changing wealth

Financial insights:

- Crypto portfolios can fluctuate wildly

- Tax planning becomes essential as gains grow

Estimated net worth trends:

- Average retail crypto investor: $1,000–$50,000 holdings

- Advanced investors: $100,000+ portfolios

With growth comes responsibility—and that includes taxes.

Common Misconceptions About Coinbase and IRS

Let’s clear up a few myths.

Myth 1: Coinbase doesn’t report anything

False. It reports certain data and complies with IRS requests.

Myth 2: Crypto is anonymous

Partially true—but traceable via blockchain.

Myth 3: Small transactions don’t matter

Incorrect. Even small gains are technically taxable.

FAQ

Frequently Asked Questions

Does Coinbase report every transaction to the IRS?

No, not every transaction directly. But it may report certain earnings and user data, and the IRS can request more information.

Do I need to report crypto if I didn’t receive a 1099?

Yes. You must report all taxable crypto activity regardless of receiving a form.

Does Coinbase report to IRS for small amounts?

It may not automatically report small amounts, but you are still legally required to report them.

Can the IRS see my Coinbase wallet?

Not directly, but they can access data through Coinbase or blockchain tracking tools.

What happens if I don’t report Coinbase taxes?

You could face penalties, interest, or audits depending on the severity.

Does Coinbase send reports internationally?

Reporting rules vary by country, but in the U.S., Coinbase complies with IRS requirements.

Is transferring crypto between wallets taxable?

No, as long as you own both wallets.

Does staking income get reported?

Yes, especially if it exceeds $600, you may receive a 1099-MISC.

Conclusion

So, does coinbase report to irs? The honest answer is yes—at least partially, and increasingly so over time.

Crypto isn’t the wild west anymore. Regulations are tightening, and transparency is becoming the norm. But that’s not necessarily a bad thing. With the right knowledge and tools, staying compliant is actually pretty manageable.

If you treat crypto like any other investment—track it, report it, and plan for taxes—you’ll avoid stress and keep your financial journey smooth.

And honestly? Peace of mind is worth it.